We are bullish gold this year in the medium term (2-6m), and likely longer term, from a macro perspective. Here’s why:

Gold has historically performed well in periods of high inflation

Gold has a -0.82 correlation with real rates, but despite coming rate hikes, inflation will outpace the fed rate, and real rates will remain negative

Gold has typically underperformed in anticipation of rate hikes and outperformed following the first rate hike of a Fed tightening cycle

Gold tends to perform well when markets have large pullbacks and outperforms the market in recessions.

*Important to note our base case assumption that the Fed raises rates. With a tight labor market, we believe they will follow through with rate hikes in the short/medium term. Significant slowing of the economy later in the year could cause the Fed to reverse direction and take a more accommodative stance.

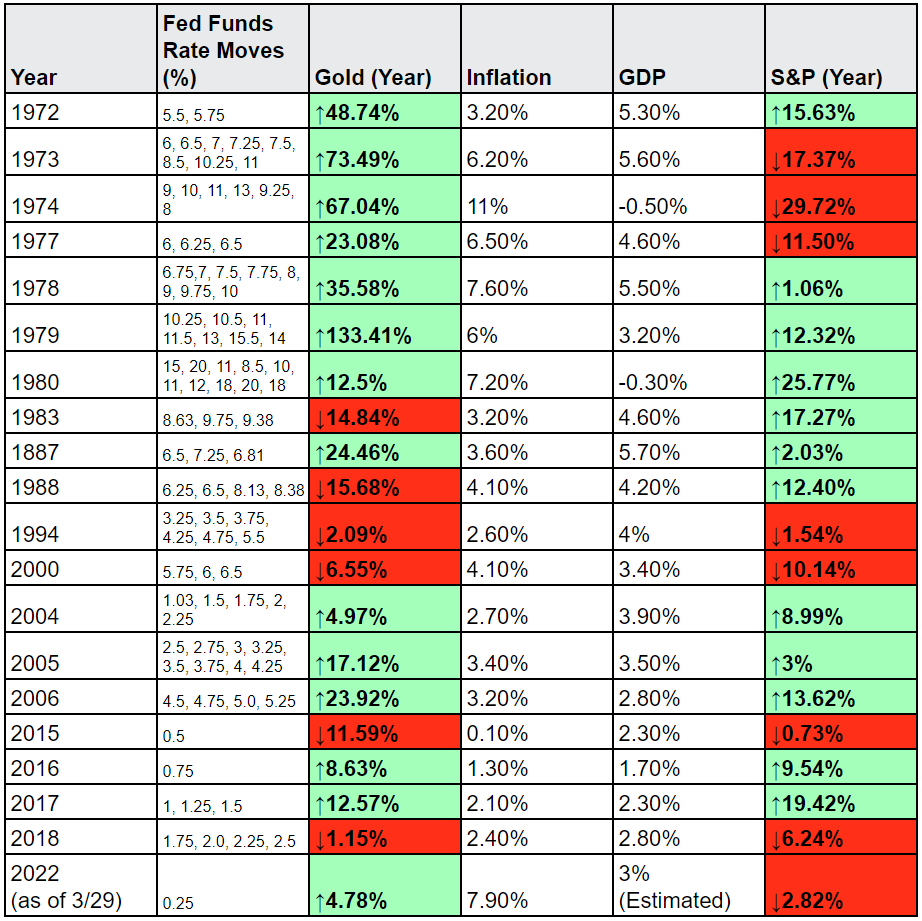

Historical Price Action of Gold in a Rising Rates Environment

In the last 50 years, when rates were raised, 14 of 19 years (74%) gold was up while S&P was up 12 of 19 years (63%), and gold outperformed S&P 12 of 19 times (63%) – gold avg return 22.82%, S&P avg return 3.36%

When the Fed has raised rates into declining growth it has been bullish for gold and when raised into accelerating growth it has been bearish (current outlook is raising rates into declining growth)

Asset Returns in Rate Hikes

Headwinds

Higher nominal interest rates

Real rates have a -0.82 correlation - When real rates go up, gold goes down

Possible stronger dollar

Russia/ Ukraine deal (temporary headwind)

Opening of supply chains drives down supply side inflation faster than expected

Tailwinds

Persistent inflation due to persistent demand and/or continued supply side pressure

Continued geopolitical uncertainty, driving up volatility

Demand from world central banks

Fear of stagflation or impending recession causing outflows from equities

Rising Rates Projections

There remains some concern that with inflation expected to come down, and rates rising, that this will put pressure on Gold, and this is very possible going forward, but we estimate that inflation readings will continue to come in at the high end of estimates for the medium term and that the fed funds target will overestimate the actual targets.

*source: Bloomberg, US Federal Reserve, World Gold Council

As seen in the graph, projections often are higher than actual. As economic growth continues to slow in 2022, we postulate that the Fed will continue to raise rates, but cautiously. Growth will suffer, and if growth is significantly below estimates, this could trigger the Fed to adopt a more accommodative wait and see policy. Furthermore, gold’s price is not only dependent on the CB moves in the US, but also in other countries, which are likely to remain more accommodative.

Supply Side Inflation

Inflation, while expected to improve, will likely linger on longer than expected. The current spike in inflation is both demand and supply side driven. By increasing rates, the Fed is only able to attempt to control demand side.

Supply side factors influencing inflation include:

China supply chain, which is again experiencing problems as China issues rolling lockdowns. The original supply shock from China was never resolved, and now new lockdowns threaten that timeline of reopening

Russia conflict and sanctions causing pressure on commodity supply and prices

Energy/Oil supply

The Global Supply Chain Pressure Index

Sources: Bureau of Labor Statistics; Harper Petersen Holding GmbH; Baltic Exchange; IHS Markit; Institute for Supply Management; Haver Analytics; Bloomberg L.P.

*Supply chain pressure remains high and will take time to untangle. It has been shown to be resolving far slower than was expected even before the new rolling lockdowns in China and the Russia conflict. Inflation will come down, and increasing rates will help, but it will remain elevated in 2022.

Historically Gold has Out-Performed S&P in Times of High Volatility/ VIX Spikes

↑↑ = >20% move ↑↑↑ = >40% move

While recession may be some time away, or never manifest, if one believes recession is coming, gold would be once again expected to outperform the S&P

Increased Demand

Gold ETF inflows- Increasing (35T in Feb)

Central Bank inflows – increasing

Asia retail demand – increasing

COMEC Net positioning – highest since Jul 2020 (as of March 1 2022)

Miners

In 2021 demand was 4,021 metric tons, while mine production was 3,560metric tons, and total supply of gold in 2021 fell 1%. Also miners in 2021 reduced aggregate hedging positions in 3 of the 4 quarters of 2021, indicating a belief that gold prices go higher. The current aggregate producer hedge is less than 150T, which is the lowest since 2014.

Total All-In Costs for production across the mining industry averages between $11,000-12,00, and any rise in the cost of gold above this, is profit for miners. Ife price of gold increases, the miners profits increase exponentially and we expect share prices, and dividends, in miners to rise accordingly

Analysts Price Targets

Specific Gold ETFs and Miners I am watching, have positions in, or trade in and out of:

*I also maintain a bullish outlook on silver in the medium term, maybe even more than gold.

Summary

I maintain that in the medium term (2-6 months) gold remains an attractive investment. The impact of rising real rates does pose a concern, but historically in a raising rates cycle gold performs well. Over the medium term, I continue to believe economic growth will slow. Raising rates into this increases the risks of stagflation. With the economic outlook, coupled with geopolitical landscape, I believe gold will remain strong. Any resolution to the Russia conflict will likely cause a pullback in gold, as will the Fed announcement of 0.5% hike. A short-term pullback in gold would not surprise and is expected. This can serve as a buying opportunity.

Totally agree good is looking good!